I have written about the basics of asset allocation. Today I would like to lay out what my own retirement asset allocation looks like.

Lazy Portfolio

I’m a set it and forget it kind of person. So the lazy portfolio works perfectly for me. I have decided on an asset allocation I can live with through thick and thin, over the long term.

What’s a lazy portfolio? Any that doesn’t require constant hovering and helicoptering for optimal results.

I do not have to stay tuned to all the noise in the market. I can go about my life and my investments will keep doing their thing. Only once in a while, if the market plunges south, (and I get to hear about it in time!), I tax loss harvest.

Target Asset Allocation

My core allocation has not changed since I first set it about six years ago.

What I was doing before then? Only individual stocks. I had never heard of Index funds. Or Vanguard. Yep, I was living under a rock.

Actually, that’s not entirely true. We had some funds in our employer-sponsored 401(k). And that infamous SEP IRA. But I couldn’t begin to tell you what their asset allocation was. It was some hodgepodge of actively managed funds. We rolled all of that into our current 401(k) and hence our current asset allocation, too.

Just this year, we do have a change in our allocation. We want to “formally” invest in real estate.

Real estate has always been part of our portfolio. But unintentionally. That story I will tell some other time.

A couple of years back, we sold those investments and used it for downpayment on our new build. That’s what kept our mortgage about 1.3x our annual household income.

So, now our investment in real estate is back down to minimal. We hope to gradually get that number up again, with time.

Target Asset Allocation

- Equities= 70%

- Fixed Income= 10%

- Real Estate= 20%

This is where I want to eventually stand.

Equity Allocation

Within that 70% allocated to stocks, 2/3 are in U.S. domestic stocks and 1/3 in International Stocks.

I am betting on the U.S. economy to continue to dominate the world economy for the foreseeable future- hence the majority in U.S. Stocks. However, the world is rapidly shrinking and I want to get in on that upside, too.

Of the 2/3 that is in domestic stocks, 2/3 of that goes into Total U.S. Stock Market Funds and 1/3 into Small Value Funds.

This is because “small” and “value” are factors that are considered to be higher risk and therefore have historically given higher returns. I have not seen this since I set my allocation. In the last decade, large growth stocks have dominated returns.

However, it’s something I am okay with continuing to do. Asset allocations are not supposed to chase performance. And, it’s a small percentage- it will not derail my retirement.

Of the 1/3 in International stocks, 80% is in Total International Stock Market Funds, 10% in Emerging Market Funds and 10% in International Small Cap Funds.

The slice and dice into Emerging Markets is to capture the momentum of smaller, faster growing economies. The small cap factor plays in the same way as in domestic. Basically, higher risk, higher return.

This boils down to:

Asset Class % of Total Retirement Portfolio

- Total U.S. Stock Market Index Funds 31%

- U.S. Small Value Funds 15.6%

- Total International Stock Market Index Funds 18.6%

- International Small Cap Index Funds 2.5%

- Emerging Markets Index Funds 2.5%

That’s it.

These funds are almost exclusively in Vanguard ETFs:

- VTI (Vanguard Total Stock Market Index Fund ETF)

- VBR (Vanguard Small-Cap Value Index Fund ETF)

- VXUS (Vanguard Total International Stock Index Fund ETF)

- VSS (Vanguard FTSE All-World ex-US Small-Cap ETF)

- VWO (Vanguard Emerging Markets Stock Index ETF)

Over time, I have tax loss harvested into “similar but not substantially identical” funds- so I have more than just these ETFs. My preferred partner ETFs are listed here.

Fixed Income Allocation

All of this is in bond funds since I do not have any cash or cash equivalents (CDs or Money Market Funds) in my retirement portfolio.

Any cash equivalents earmarked for Emergency Fund or towards short term goals, which I wouldn’t want in the market, are not part of this discussion.

All of this bond allocation is in a Defined Benefit Plan/Cash Balance Plan at work and this is how it looks:

- Intermediate Term Treasuries= 50%

- Short Term Treasuries= 30%

- Inflation Protected Securities= 20%

Real Estate Allocation

This is a work in progress. Currently I’m thinking 20% in publicly-traded REITS and 80% in Passive Real Estate, such as Private Real Estate Funds and Syndications. However, if we ever feel we can make the time for active real estate, those proportions will change.

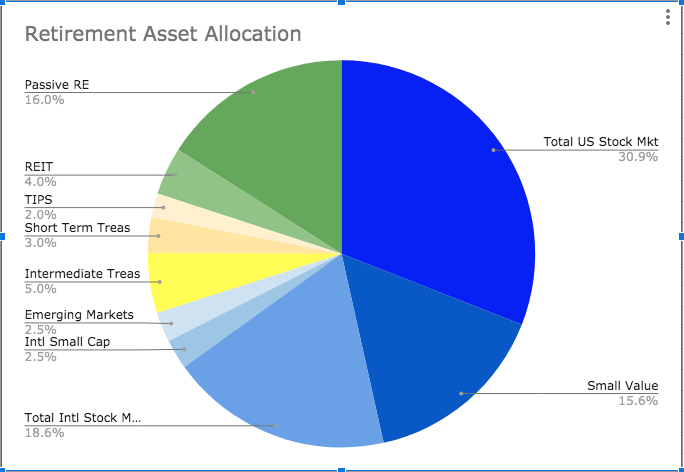

All in all, this is what it boils down to:

All the blues are Equity allocations, all the yellows are bonds and the greens are Real Estate.

My Current Asset Allocation

Among my equity allocation, I’m pretty close to target.

The Total U.S. Stock Market is at more than target because it has rapidly climbed in this bull market and has consistently beaten U.S. Small Cap Value stocks, which is therefore below target, for me.

This is despite all new money going towards the underrepresented, which is my preferred rebalancing method.

The International holdings are pretty much on target.

My bond allocation is rapidly growing, more than I want it to. This is because we have a stellar Defined Benefit Plan, which lets us put in a huge chunk of pre-tax money every year.

To counter that, I need to put in a proportionate amount into stocks. But my savings rate has been lower in the last couple of years because we’re building the house and that thing costs a pretty penny. We’re cash flowing some of it to keep the mortgage at a comfortable level.

Hopefully by next year, we’ll be done with the build and get our savings and that stock allocation back up again.

In the meantime, the high bond allocation is tempering the increased risk of the real estate holdings, for better or worse.

Asset Location

I put the most tax inefficient asset classes in tax-advantaged accounts and then let the other spill over into taxable accounts, if they must.

So, the REIT Fund, and most of the Small Value Funds, Emerging Markets and International Small Value holdings are in tax-protected space.

Much of the Total Market Index Funds, both domestic and International is in taxable accounts. The International Funds also lets me earn a small Foreign Tax Credit.

Some Small Value funds and some Emerging Market Funds are in taxable- and they have presented some great tax loss harvesting opportunities.

Blast from the past

What about those pesky individual stocks I began my investing career with? Well, they’ve done very very well in this long running bull market and ballooned to higher than I’d imagined.

So I don’t include them in my retirement portfolio anymore. Otherwise they’d skew the asset allocation horribly.

It’s fun money and if it goes poof! one day, I’ll have miss it but it won’t screw up our retirement plans.

I’ve often wondered whether I’d like to take some of it off the table- and play only with house money. But I don’t have enough accumulated losses to offset the gains. Once I get to tax loss harvest some more, maybe I’ll do just that.

Drawbacks of my Retirement Asset Allocation

- It is a lazy portfolio but could be lazier. And I’m pretty sure my returns wouldn’t know the difference. But the complexity introduced by this small amount of slice-and-dice doesn’t bother me (yet).

If at any stage, it becomes a bother, I can eliminate a couple of asset classes.

If for example, in a couple of decades, I want to simplify things for myself. Or if I croak unexpectedly and my husband is managing things, I’d want it to be as simple as possible.

The Emerging Markets and International Small Cap Funds might be first on the chopping block. The Small Value sector allocation may be next.

- I’m not rebalancing with great precision. That would require selling of assets. And I don’t like to bother with that. I rebalance with new money going towards the asset class that needs catching up.

I have justified this selective laziness since rebalancing is apparently of dubious benefit, as per a Vanguard study.

- It is an aggressive allocation. And as we get closer to retirement, over the next couple of decades, we will need to tone it down. I still want to stay at over 50% in stocks, since both Bengen’s Study and the Trinity Study have found that the best returns come from an equity allocation between 50-75%, even during the retirement years.

Thoughts and comments? How does your asset allocation look? Let me know below. And thanks for reading!